Daily Chartbook #12

30 charts

Welcome to PAV Chartbook: market charts, data, research, and insights pulled from various sources around the Internet by a solo retail investor.

1. Pump relief. The cost for a gallon of gas has declined for 50 days straight (from outrageously high levels). The national average is at $4.16 a gallon.

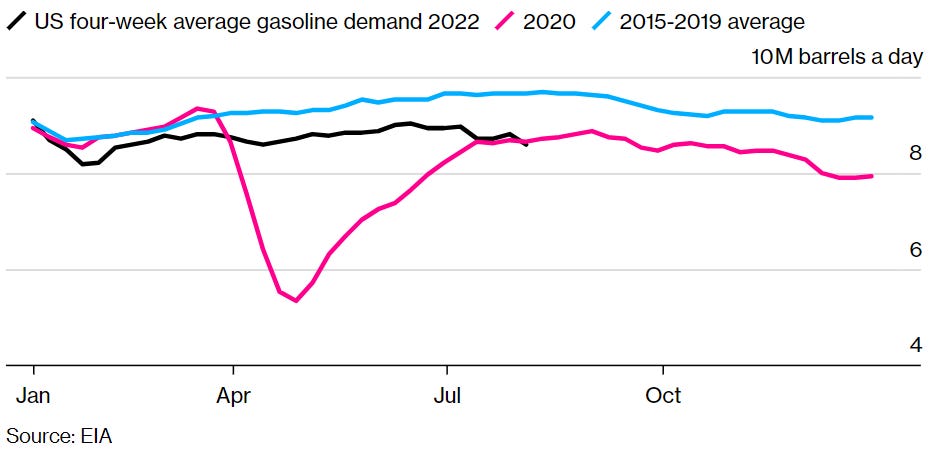

2. Less gas demand now vs. peak pandemic. A combination of higher prices and Work From Home is resulting in less drivers?

3. US inventories. Total US petroleum inventories rose by ~3.5 million barrels last week but remain within the lower bounds of their 5-year ranges, or below them outright.

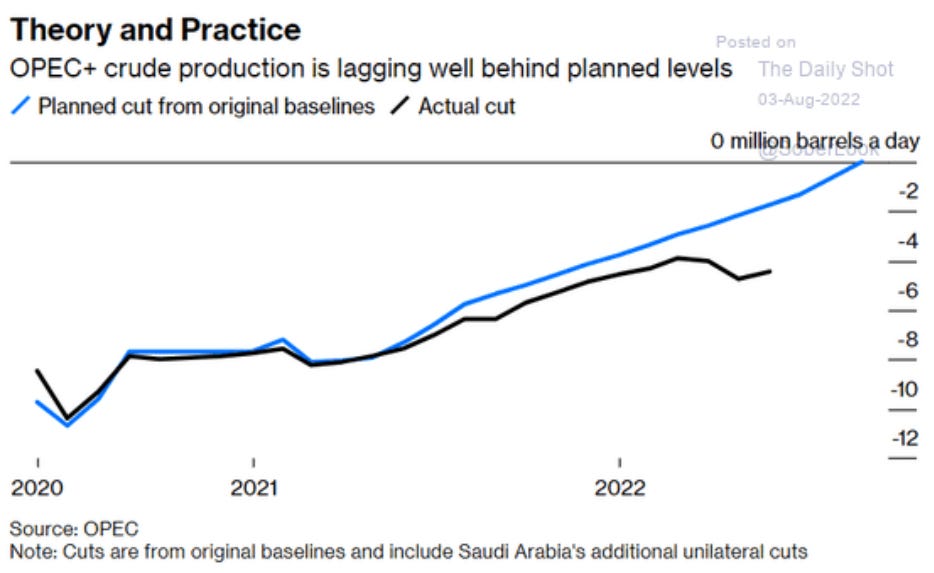

4. Biden strikes out. The Oil Cartel (OPEC+) has already consistently failed to follow through on promised output levels. Today it proposed an increase of 100,000 barrels per day in September…this is the second smallest increase in history.

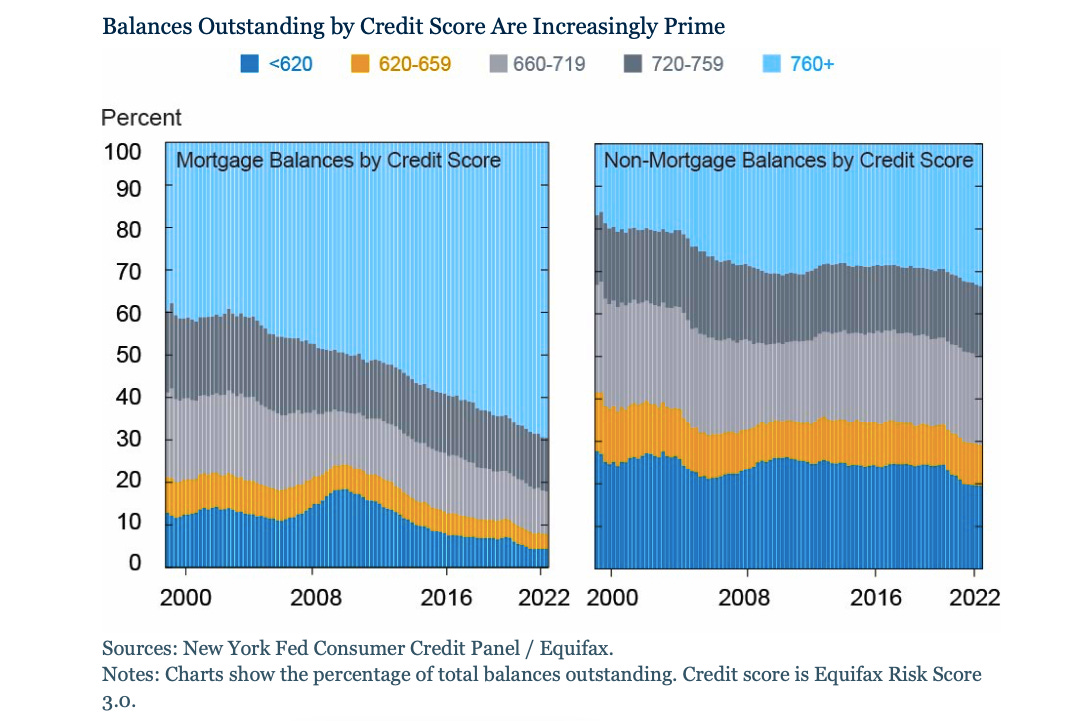

5. Delinquencies up. We’re seeing an uptick in credit card and auto delinquencies.

6. Higher quality borrowers. On the other hand, “lenders have been much more disciplined with their lending practices. A growing share of debt being issued is going to borrowers with high credit scores”.

7. Q3 GDP. Goldman Sachs is estimating GDP growth of 0.9% in the third quarter.

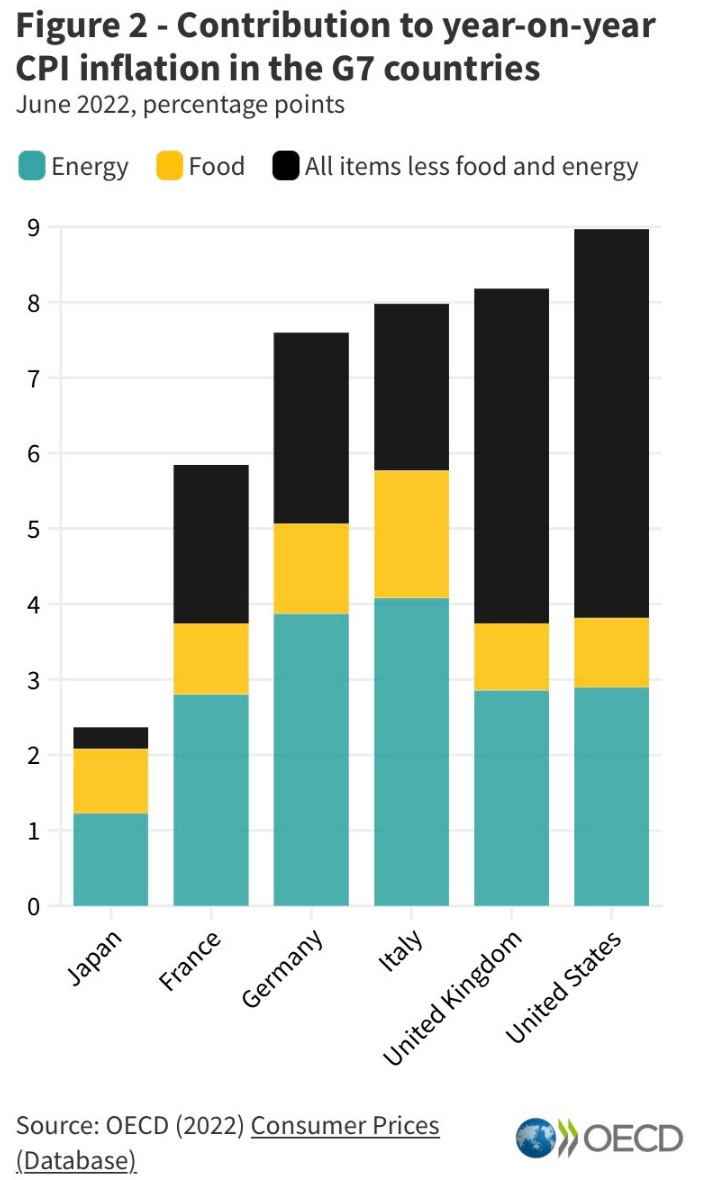

8. G7 inflation. Here’s how much the volatile energy and food categories have contributed to inflation in the G7 countries (sans Canada).

9. Supply chain snarls subside. “The Baltic Dry Index, a key measure of global shipping costs, is back at its long-run mean as supply disruptions continue to ease.”

10. ISM Services PMI up. The ISM Non-Manufacturing PMI rose unexpectedly in July by the most in 3 months. The Business Employment contracted for the second straight month, but at a softer rate.

11. ISM Services Prices Paid down. The prices paid index dropped in July to its lowest level since February 2021—a positive sign for easing inflation.

12. ISM Prices Paid & Inflation. The drop in ISM prices paid (an average of manufacturing and services) has yet to be reflected in headline inflation.

13. ISM & S&P 500. Here’s the S&P’s price overlaid with ISM Manufacturing and Services Activity.

14. S&P Global US Services PMI surprises down. On the same day that ISM Services PMI expanded more than expected, another gauge for services activity surprised us with its first contraction since June 2020.

15. Factory orders strong. New orders for US manufactured goods rose for the 9th straight month and nearly doubled market estimates with 2% growth in June.

16. Orders divergence. “And notably, this factory orders increase comes as ISM's survey show manufacturing orders tumbling? Perhaps the survey is 'real' (inflation adjusted) and the hard data is nominal? Or the survey is just a sign of ugly things to come (like in 2007).”

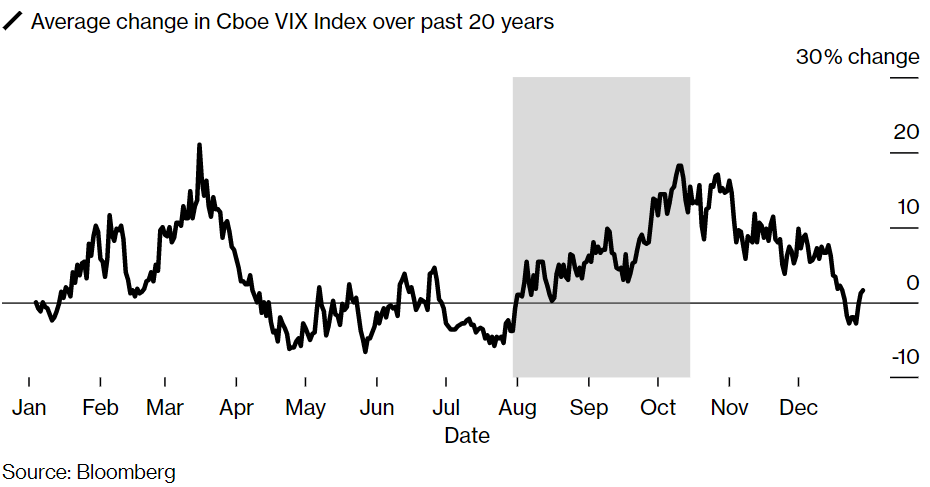

17. Volatility ahead? “Seasonality suggests volatility might rise until end of summer”. So far VIX hasn’t gotten the message.

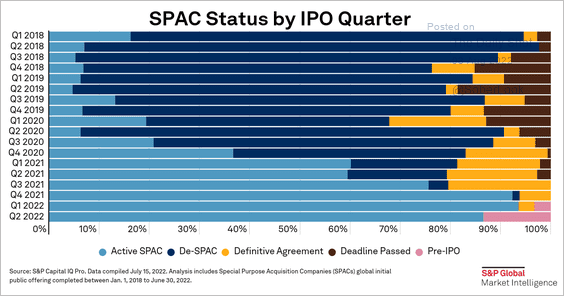

18. SPAC check. Remember special-purpose-acquisition-companies?

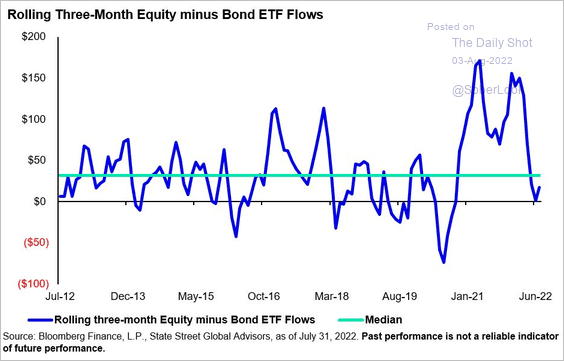

19. Equity vs Bond ETFs. “Equity ETF inflows were well below historical averages last month, while bond funds attracted fresh capital.”

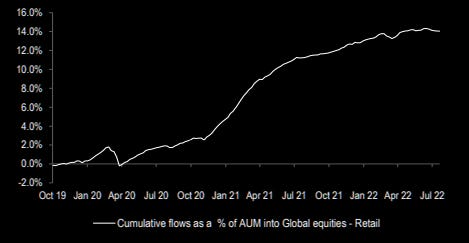

20. No capitulation from retail. Global retail investors have held the line

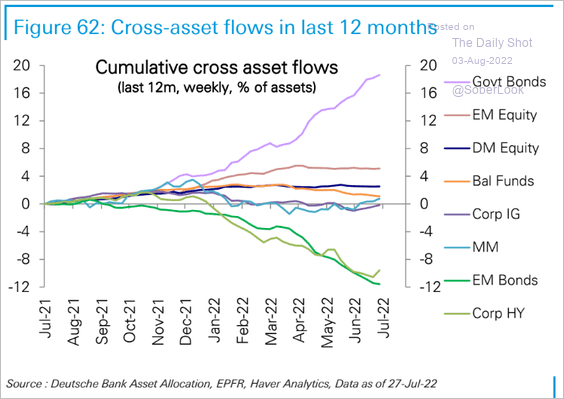

21. Fund flows. Where the money has gone over the last year.

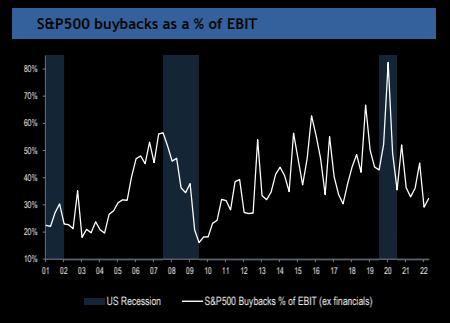

22. Buybacks. As they relate to profits, stock repurchases remain low.

23. S&P earnings. “With 67% of S&P 500 companies having reported, 69% are beating 2Q earnings (vs. 79% avg. last 4Qs) and 65% are beating revenue estimates (vs. 77%)” - JPM

24. Lion’s share. The top 10 stocks in the S&P 500 used to account for ~34%. of the index’s earnings. That’s down to 20%. They still command nearly 30% of the market cap.

Top 10 stocks by market cap: AAPL 0.00%↑ MSFT 0.00%↑ AMZN 0.00%↑ TSLA 0.00%↑ GOOGL 0.00%↑ GOOG 0.00%↑ $BRK.B UNH 0.00%↑ NVDA 0.00%↑ JNJ 0.00%↑

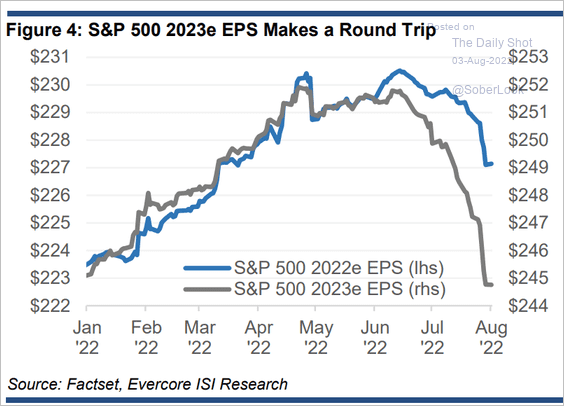

25. S&P earnings. Will EPS estimates continue falling?

26. Growth vs. Value (I). Growth stock valuations are on the rise but are well below the exuberant levels prior to 2022.

27. Growth vs. Value (II). Growth stock prices are also beginning to reverse their relative underperformance against value stocks.

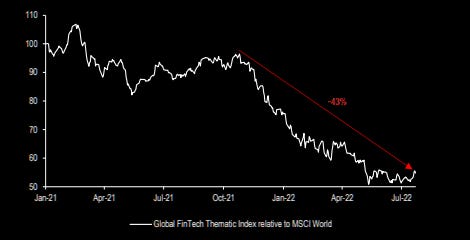

28. Growth vs. Value (III). Not all growth stocks though…

29. S&P operating margins. The S&P 500 isn’t buying the drop in forward operating margins (yet?).

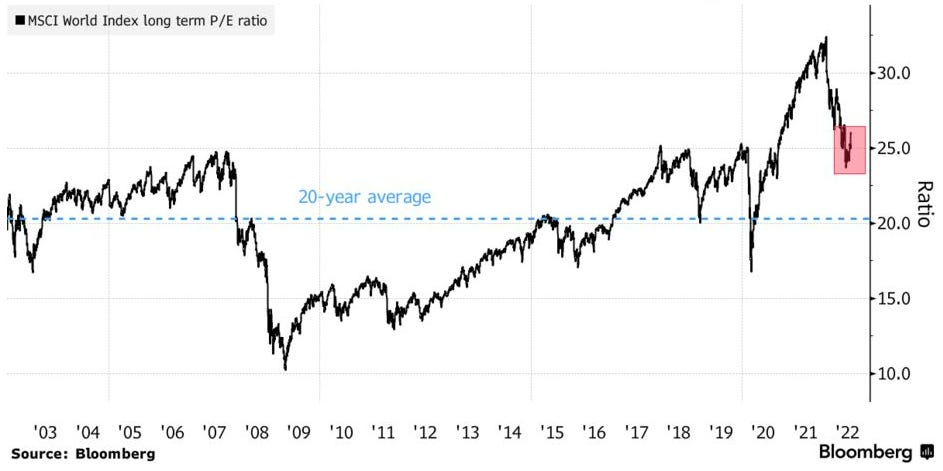

30. Global P/E. And finally, yesterday we noted that the S&P 500 was “near its average year-end P/E ratio (since 1989) of 19.6”. Valuations don’t look so attractive when considering global stocks, where the P/E ratio remains well above the 20-year average.