Daily Chartbook #26

Catch up on the day in 32 charts

Welcome back to Daily Chartbook: market charts, data, research, and insights pulled from various sources around the Internet by a solo retail investor.

1. Natural gas (I). German electricity costs have surpassed the equivalent of $1,000 per barrel.

2. Natural gas (II). "US natural gas prices rose above $10 per million British thermal units for the first time since 2008" yesterday. Prices moved back down today after Freeport LNG delayed plans to restart its Texas export terminal from October to November.

3. Natural gas (III). US natural gas inventories are 12.7% below typical levels for this time of the year.

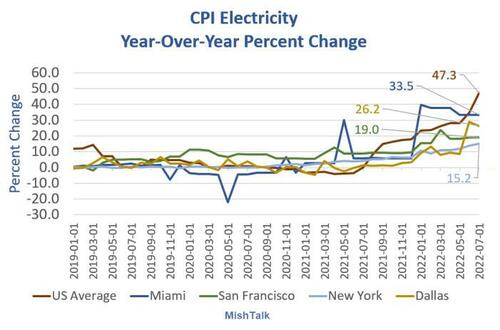

4. Electricity CPI. "The average US household pays 47% more for electricity than a year ago".

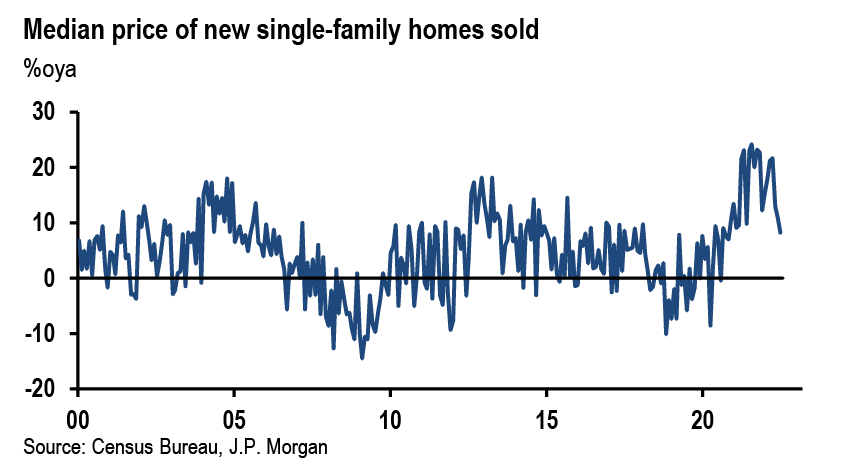

5. New home sales (I). New home sales fell 12.6% in July while the median sales price for new homes rose to $439,400. The average sales price was $546,800.

6. New home sales (II). The rate of price growth for new homes is slowing.

7. New home sales (III). New home sales are down over 30% YoY.

8. New home sales (IV). They have also “hit a 6-year low in July, down over 50% from their 2020 high”.

9. New home sales (V). The breakdown of sales by region.

10. New home sales (VI). New home sales contributions by region (MoM).

11. New home sales (VII). Months supply of new homes increased sharply in July.

12. Supply chain. The Baltic Dry Index is at its lowest since December 2020 reflecting an easing freight market, "mostly due to lower Chinese demand".

13. Restaurant customer traffic. "Customer traffic subcomponent within National Restaurant Association’s Restaurant Performance Index has slipped into contractionary territory for first time since February 2021".

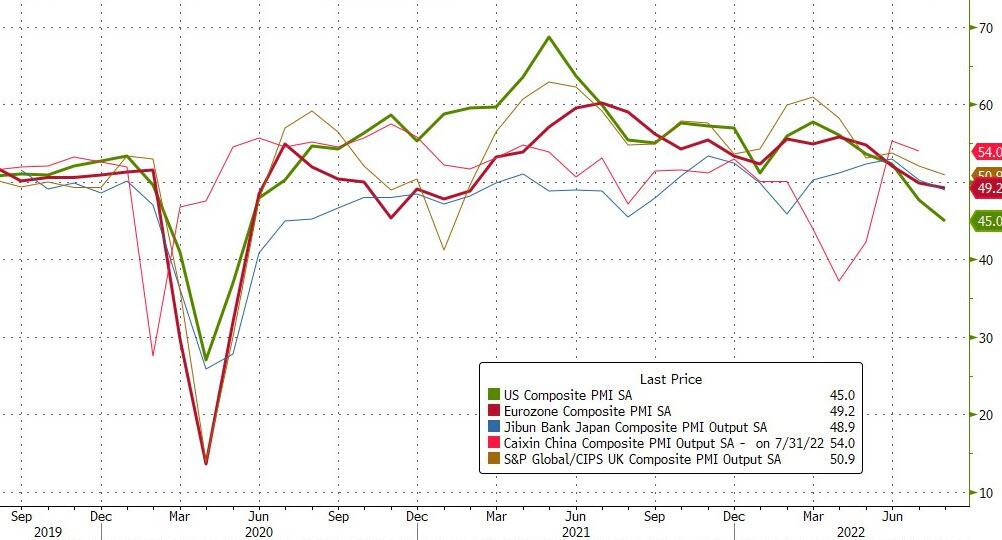

14. Eurozone PMI (I). Eurozone Flash PMI dropped to 49.2 in August, "signaling a reduction in business activity as the cost-of-living crisis sapped demand for services."

15. Eurozone PMI (II). The only times the Eurozone's New Orders to Inventory Ratio have been lower was during the Global Financial Crisis and the pandemic.

16. Food prices. Global food prices are still elevated but down from extreme levels.

17. Q3 GDP. Goldman increased its estimate for GDP growth to 1.3% for Q3 to reflect the positive retail sales and industrial production reports.

18. Positive surprises. Goldman's economic surprise index has been moving up since June and is now in positive territory.

19. American morale. The number of Americans who say they are "thriving" is at an 18-month low.

20. Flash PMI (I). US business activity declined at the fastest pace since May 2020 as the S&P Global US Composite PMI declined to 45.

21. Flash PMI (II). Both manufacturing and services PMI fell more than expected. They are at their lowest since July 2020 and May 2020, respectively.

22. Flash PMI (III). "The US Composite PMI is the weakest of all the global regions".

23. Richmond Fed. The Richmond Fed Manufacturing Index fell back into contraction territory as shipments and volume of new orders both dropped sharply.

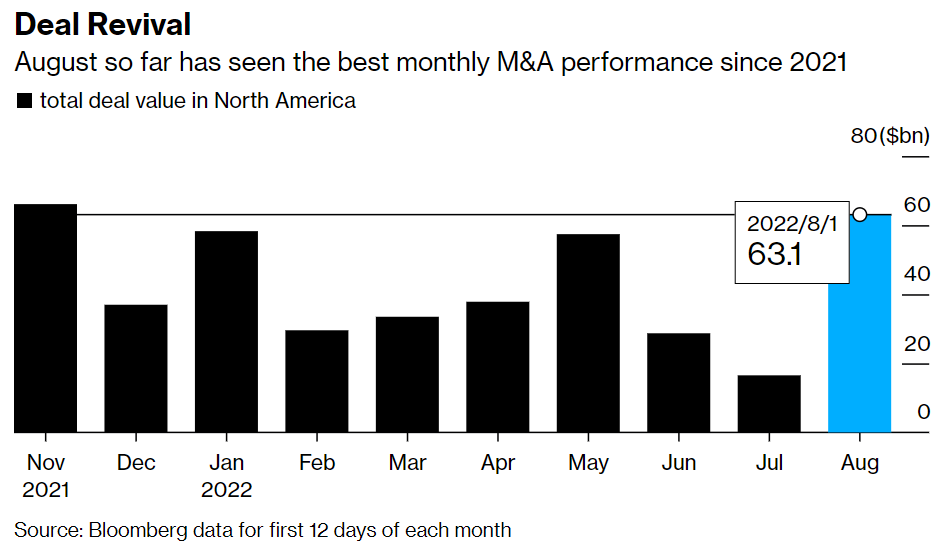

24. Hot M&A. Mergers and acquisitions are down in 2022 but August has been the most active month of the year with $63 billion in transactions announced in North America.

25. Takeover targets have outperformed. "The basket includes stocks that GS analysts believe have at least a 15% probability of M&A activity over their price target periods. The basket has outperformed the S&P 500 by 16.2% YTD."

26. Stocks & bonds. "The correlation between stocks and bonds over the last 2 years is the highest we've seen since 1995-1997."

27. Cheap cyclicals. On a forward P/E basis, cyclicals are cheap relative to the S&P 500.

28. Low volume theme. Today’s trading volume was among the lowest of the year.

29. Bearish positioning. Combined positioning between leveraged funds and asset managers is bearish.

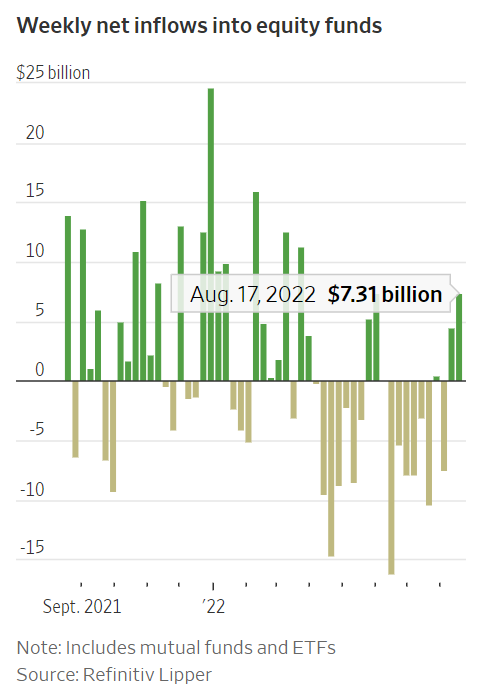

30. Big equity inflows. Investors bought a "net $11.7 billion into equity mutual funds and exchange-traded funds over the two-week period ended last Wednesday".

31. EPS growth 2023. S&P 500 earnings excluding energy are expected to grow an optimistic 9.3% next year.

32. And finally...Bull or Bear? Either way, there's a chart for you.