Daily Chartbook #38

Catch up on the day in 28 charts

Welcome back to Daily Chartbook: macro market charts, data, and insights pulled from various sources around the Internet by a solo retail investor.

1. Mortgage rates (I). "The 15-year mortgage rate in the US rises to 5.16%, its highest level since December 2008. A year ago it hit an all-time low of 2.10%".

2. Mortgage rates (II). "Adjustable Rate Mortgages in the US move up to 4.64%, the highest rate since 2009. At the end of last year they hit an all-time low of 2.37%."

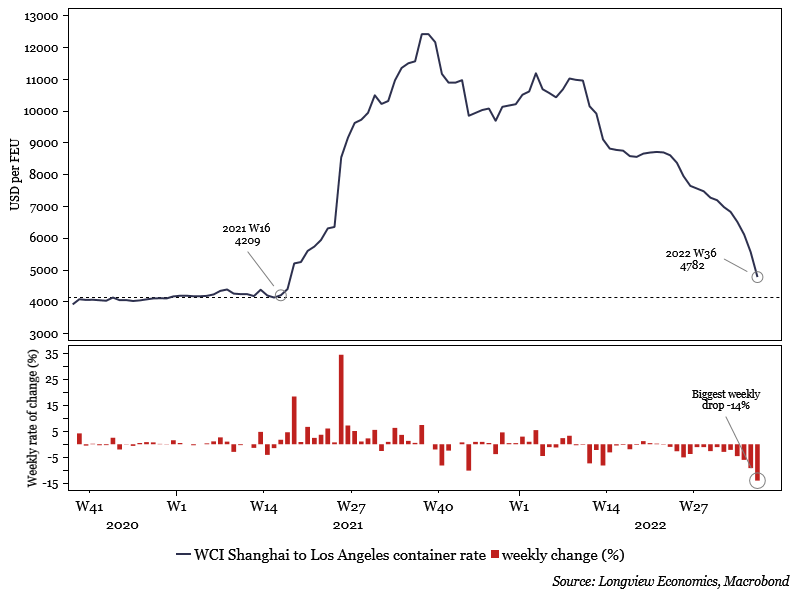

3. Shipping rates continue improving. "Biggest weekly drop yet in ocean freight rates (-14%)."

4. Snarls are subsiding. Citi's Global Supply Chain Pressures Index continues to improve as well.

5. Global sentiment. Global consumer sentiment has collapsed.

6. Global outlook. Here's Citi's recession outlook for major countries.

7. PPI: China vs US. A drop in China's producer prices (blue) suggests relief for prices in the US (red).

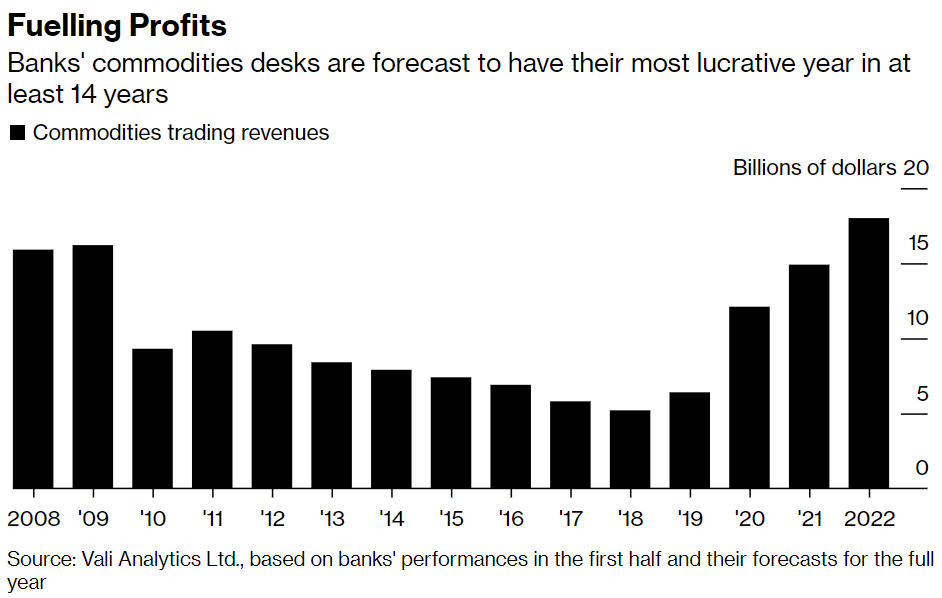

8. Commodity traders. The world's biggest banks are on track to generate the most revenue from commodities trading ($18 billion) in at least 14 years.

9. Household spending. From "BofA: Discretionary spending growth rebounded in August after contracting in July".

10. Household balances. Customer savings and checking accounts are still well above pre-pandemic levels.

11. Household net worth. On the other hand, US households lost $6.1 trillion in net worth last quarter—mostly due to lower stocks—for the largest quarterly drop ever.

.")

12. 2023 payrolls forecast. "BofA expects job losses for much of next year".

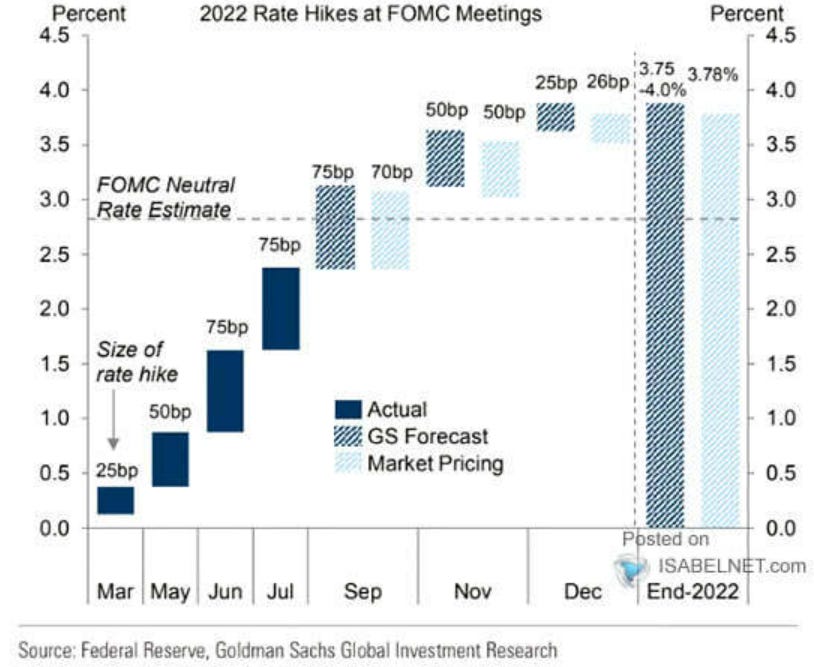

13. Rate hikes forecast. Goldman predicts the Fed will raise by 75 bps this month followed by another 50 bps in November and 25 bps in December.

14. US bankruptcies are down. Through August, there have been just 249 corporate bankruptcies in the US—the lowest amount over the period since 2010.

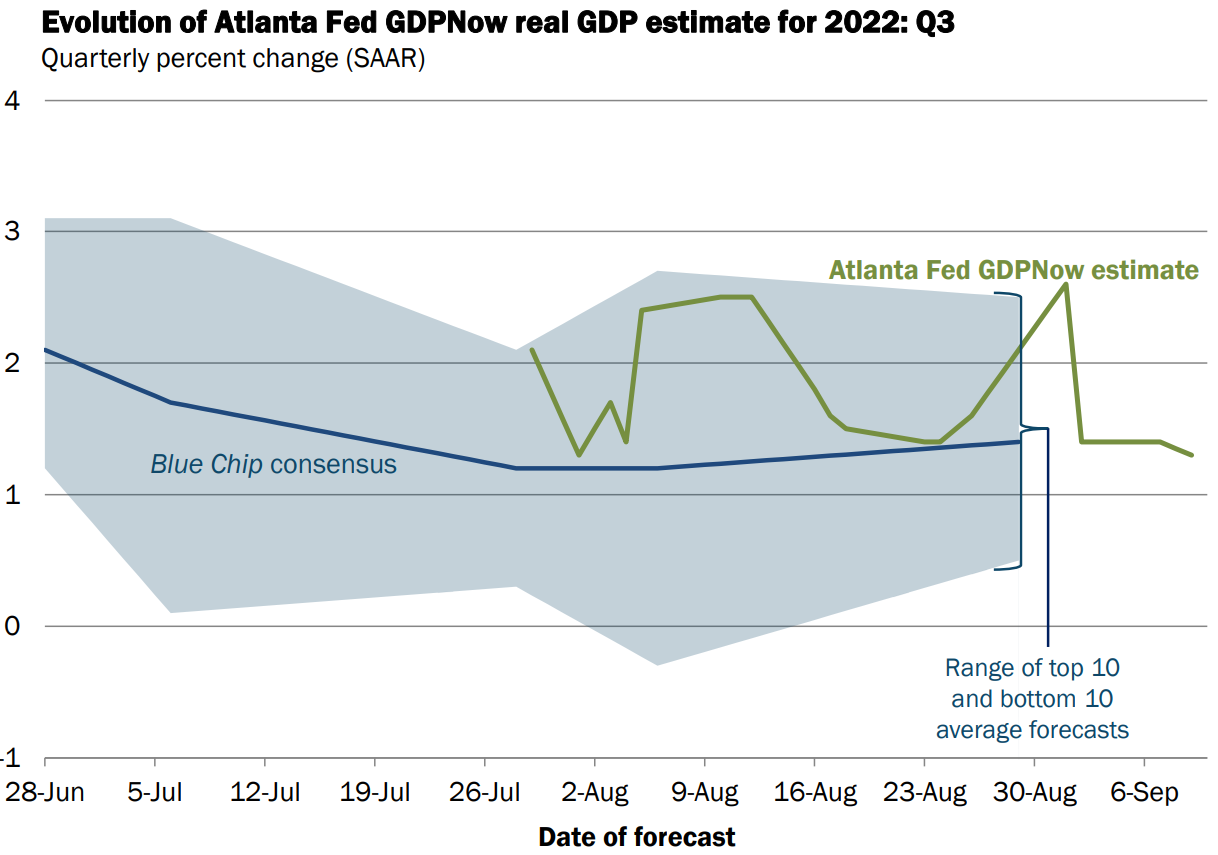

15. Q3 GDP. Atlanta Fed's GDPNow estimate dropped to 1.3% from 1.4%.

16. US regimes. Where we are in the cycle, according to BofA.

17. Banks are tightening. US banks are tightening lending standards which suggest a drop in earnings.

18. Low liquidity. "A lot of chatter about risk assets moving back up, but with financial conditions tight, inflation elevated, and QT on full force excess liquidity is low and falling."

19. Flows (I). "CTA one week net change in positioning is one of the largest net selling in US equities over the last 5 years".

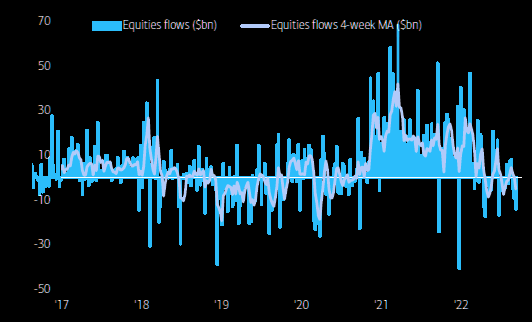

20. Flows (II). Equity outflows spiked to $10.9 billion in the week ending September 7 (largest since June).

21. Flows (III). Tech stocks saw their largest outflows ($1.8 billion) since January 2019.

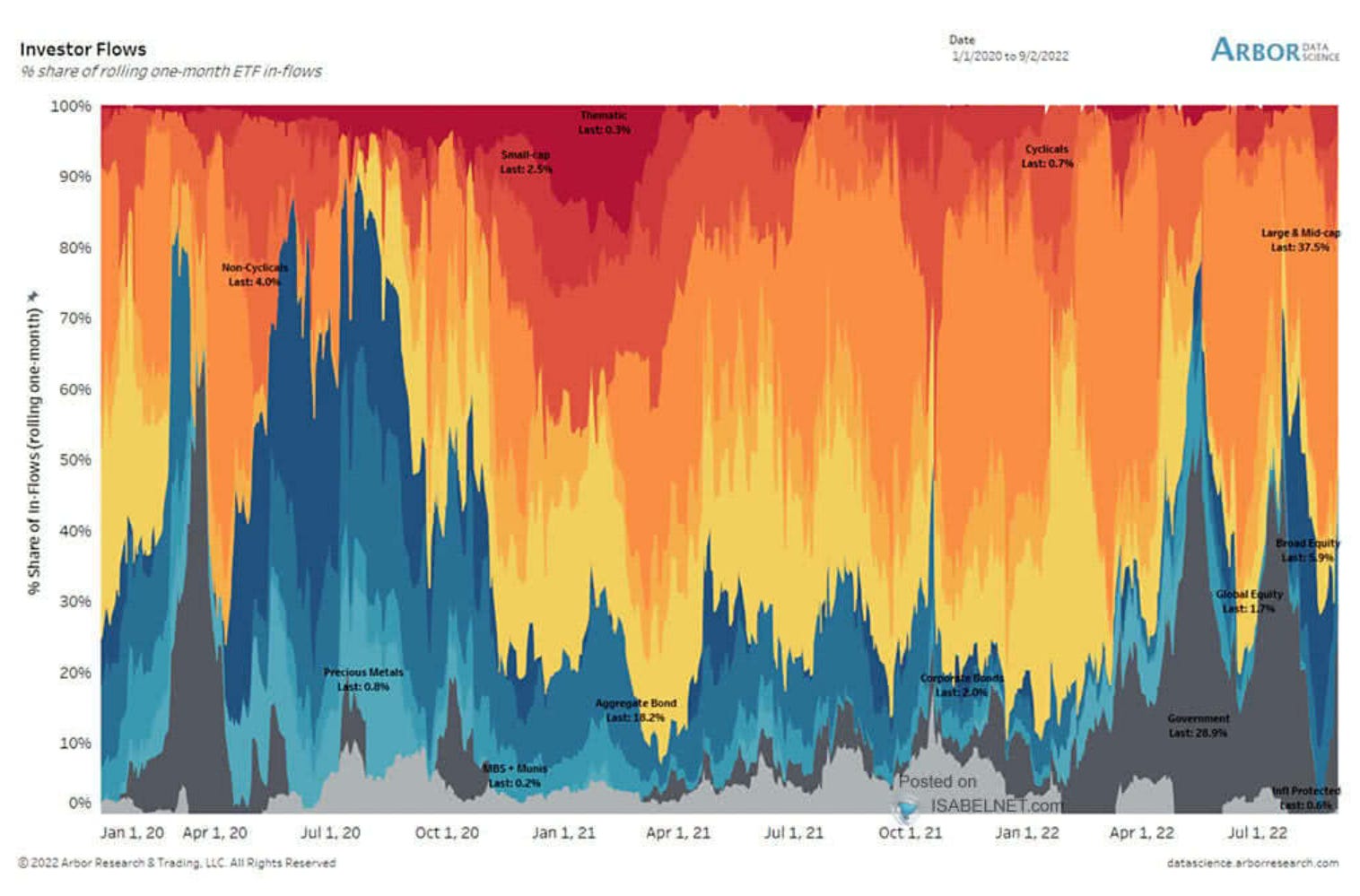

22. Flows (IV). Rolling one-month ETF inflows suggest investors remain risk-on. Large & mid-cap funds account for 37.5% of inflows.

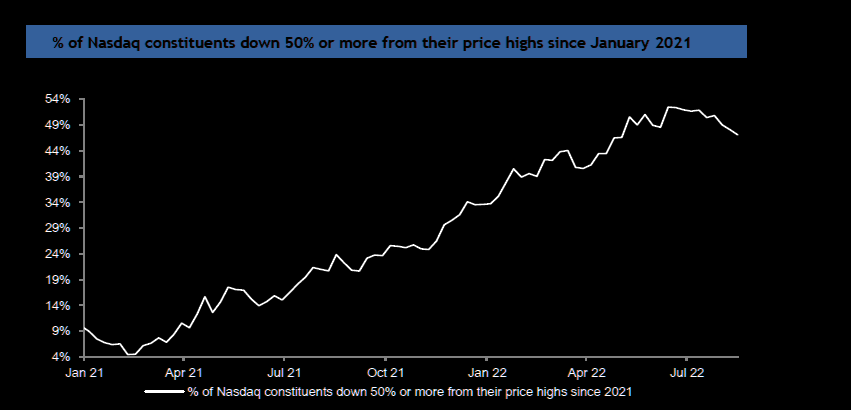

23. Nasdaq is on sale. "Almost half of Nasdaq constituents are trading at least 50% down vs 2021 highs".

24. S&P 500 valuation. "The S&P 500's forward price-to-earnings ratio is back above its long-term [20-year] average".

25. 2022 winners & losers. "The best and worst performing stocks in the S&P 500 this year".

26. 2022 EPS estimates. Consensus earnings estimates are approaching 0% growth.

27. Trouble head? "Historically speaking, the weakest time of the year for the S&P 500 has been from September 6 to October 25."

28. Recession talk. And finally, more S&P companies cited "recession" during Q2 earnings calls than any other time in at least 10 years. Here's the breakdown by industry.

Have a great weekend!