Welcome back to Daily Chartbook: macro market charts, data, and insights pulled from various sources around the Internet by a solo retail investor.

1. Strategic Petroleum Reserve. Last week, the White House made its biggest ever release since the creation of the SPR with 8.4 million barrels sold.

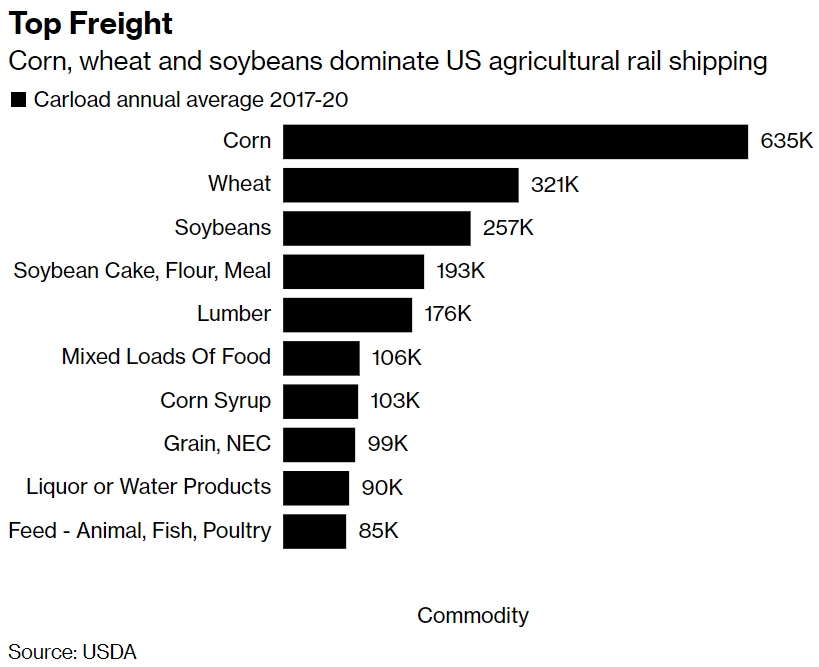

2. Railroads (I). "Railroads are already seeing delays. With a possible worker strike starting Friday 16 Sep, things can only get worse".

3. Railroads (II). "A strike would threaten shipments of grains, fertilizer and energy when global food prices are elevated and inflation ripples through economies".

4. Recession talk. The frequency of the topic of "recession" in the news has declined but remains very high.

5. Consumer expectations. "Consumers’ expectations for income growth (blue) has climbed to new high, while expectations for home price growth (orange) have plummeted".

6. Headline & core inflation (I). Both headline and core inflation came in hotter than expected, rising by 0.1% (vs. -0.1% expected) and 0.6% (vs. 0.3% expected), respectively.

7. Headline & core inflation (II). Headline and core inflation are now 8.3% and 6.3% YoY, respectively.

8. Topline contributors to inflation. A big drop in energy prices was overwhelmed by an increase in all other categories.

9. Inflation subcomponents. Breakdown of MoM percent change in top 5 subcomponents.

10. Big drop in energy prices. The energy component declined by 5.5% YoY in August, the "largest contraction since April 2020".

11. Food inflation. The food component rose by 11.4% YoY in August, the "fastest rate since April 1979".

12. OER inflation. The owners' equivalent rent (OER) component rose by 6.3% YoY in August, the "fastest increase since April 1986".

13. Inflation by category. Year-over-year change for select CPI categories.

14. Biggest problem. Inflation was still the single biggest problem for small businesses in August by a wide margin.

15. CPI vs. Fed. In the past, the Fed has hiked interest rates beyond the rate of inflation to reel in prices.

16. Market expectations. “The market is now pricing in Fed rate hikes to 4.25%-4.50% by the first quarter of next year, then rate cuts in the back half of 2023 and more cuts in 2024”.

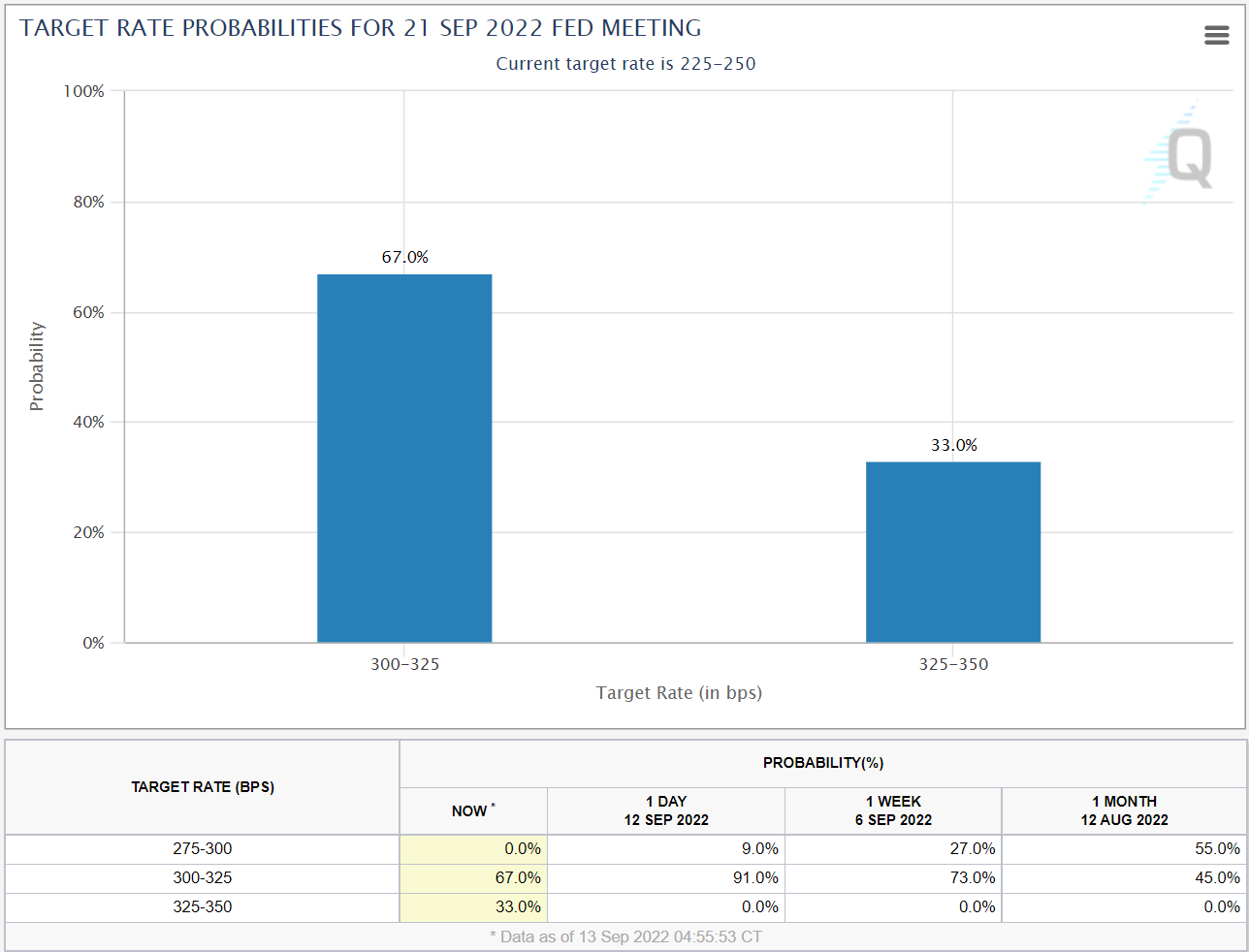

17. 100 bps? After today’s inflation print markets put a 33% probability on a full percentage-point increase in rates.

18. Net buyers. "Last week, during which the S&P 500 was +3.6%, clients were net buyers of US equities ($3.8B) for the first time in four weeks, with flows into both stocks & ETFs."

19. Light positioning. Systematic (blue) and discretionary (green) equity positioning are in the 9th and 13th percentiles, respectively.

20. Risk-off. "Most market sentiment indicators remain risk-off".

21. Macro options. "Index options continue rising while single stock options continue falling".

22. Global Fund Managers (I). More fund managers are underweight global equities than ever.

23. Global Fund Managers (II). Fund managers "are short equities and long Cash."

24. Global Fund Managers (III). “Long US dollar remains the most crowded trade.”

25. Global Fund Managers (IV). Fund managers also see the USD as the most overvalued on record. Conversely, they see other currencies as the most undervalued on record.

26. Global Fund Managers (V). "Highest amount of cash as percentage of the assets under management since 2000".

27. Global Fund Managers (VI). And finally, "the risk appetite is at the lowest level seen in 20+ years, even lower than the 2008 crash".