Daily Chartbook #7

23 charts

Welcome to PAV Chartbook: market charts, data, research, and insights pulled from various sources around the Internet by a solo retail investor.

1. Gas rationing in Germany is inevitable. “Germany's gas storage levels usually make it to 90% by late autumn. That gets Germany through the winter with Nordstream running at 100%. But Nordstream now is running at only 20%, so - even if storage levels were to somehow get to 90% - it just isn't enough. Rationing is coming.”

2. O&G FCF. The world's biggest oil & gas companies are generating record amounts of free cash flow.

3. Travel plans. Americans are not letting high prices get in the way of their vacations and 68% are not letting anything stop them.

4. Global shipping. Prices for shipping goods via air are dropping along major routes.

5. Tight inventories. Inventories of finished products around the world are below desired levels.

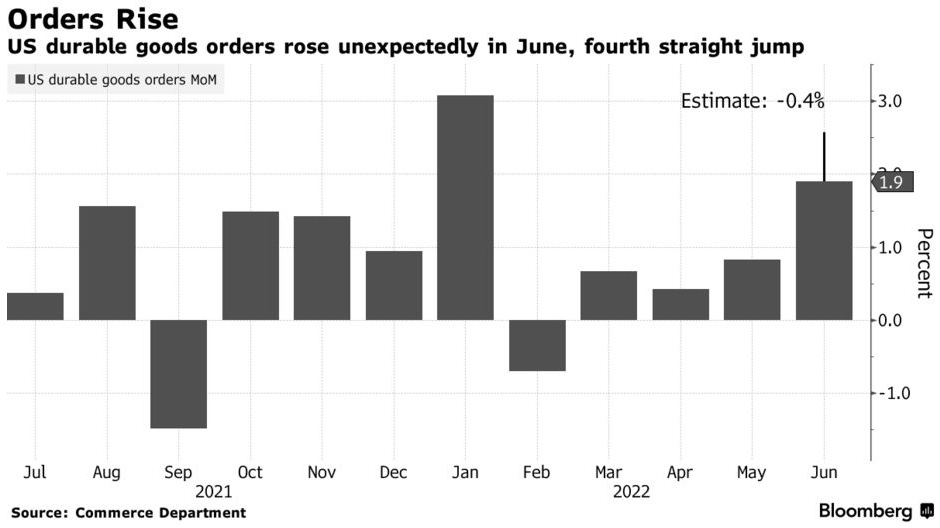

6. Durable goods. New orders for durable goods jumped unexpectedly in June. It’s the 4th straight increase and the 8th in the last 9 months. The 1.9% rise topped estimates of a -0.4% decline for the 2nd biggest rise of the year (January). The increase was “fueled by a surge in defense aircraft as well as sustained demand for equipment”.

7. Business spending plans. Orders for non-defense (core) capital goods excluding aircraft—which is used as a proxy for business private business spending—remain strong, increasing 0.5% in June.

8. Fed funds rate & financial conditions. “Financial conditions have tightened by the equivalent of 283bp in fed funds since the start of 2022.”

9. Money supply. The M21 money supply just experienced its largest 3-month decline in nearly 20 years. Will this result in a more dovish Fed?

10. Expectations. Also coming down are consumer inflation expectations thanks to falling gas prices.

11. Atlanta Fed. The final Q2 GDPNow estimate was released this morning. It predicts tomorrow’s GDP growth rate will be -1.2%. Last week the estimate was -1.6%.

12. BEA is more optimistic. The Bureau of Economic Analysis doesn’t think we’re in a recession, estimating GDP growth of 0.4%.

13. Goldman Sachs is more positive. The Wall Street giant is even more bullish on the US economic outlook, predicting growth of 0.5% in Q2 followed by 2.5% growth in H2 2022.

14. FOMC: They were who we thought they were. The Fed raised interest rates by the expected 75 bps this afternoon. Here’s a history of Fed hikes including today.

15. FOMC tone. Here are the changes made from the committee’s last statement.

16. Earnings peak. Tomorrow will be the busiest day of earnings season with over $9.4 trillion in market cap reporting highly anticipated numbers.

17. Sectors under pressure. Companies have been reporting a dip in margins (excluding energy).

18. Volatility. Meanwhile, VIX is laying at its lowest since July 2019.

19. Tech-heavy. Technology stocks led the way today. They currently account for more than 25% of the S&P 500.

20. Hotel stocks. Remember the travel figures above?

21. Big ETF flows. “At the half-year point, US investors had already added $212 billion to equity ETFs. That’s above full-year levels for 2016, 2018, and 2019, & not far off 2020’s $241 billion. At this pace, annual equity #ETF flows will be the 2nd highest ever, behind 2021.”

22. The circle of life. “Looking at 22 major segments of the equity market, outperformers in one decade became underperformers over the next decade over every rolling period, starting with the comparison of 1990-1999 and 2000-2020. In fact, an average of 6.0% of outperformance from the winners in the starting decade became an average of 2.8% of outperformance from the prior losers in the next.”

23. Not that bad. And finally, from a price perspective (and outside of communication services) “most sector drawdowns have been tame vs former recession bear markets (thru 6-15-22)”.

“M2 is a measure of the money supply that includes cash, checking deposits, and easily-convertible near money.” - Investopedia